.jpg)

Introduction

For much of crypto’s existence, trading on permissionless blockchains won on access and lost on execution. Markets were composable, transparent, and easy to build on. However, they were not the best execution venues, and as a direct consequence offered worse prices to users. That was the necessary tradeoff of decentralization, or at least it was widely assumed to be. If you wanted tighter spreads, faster repricing, and more sophisticated market making, the belief was that you had to move backwards toward closed or permissioned systems.

If the first era of onchain markets was defined by that assumed tradeoff, the current era will be defined by breaking it. We believe permissionless blockchains have reached the point where the market structures built atop them can not only provide comparable execution to centralized exchanges but outcompete them entirely. Today PropAMMs on Solana are the first evidence of that new beginning.

The (Onchain) Evolution So Far

The first generation of passive AMMs solved a real market-structure problem; they made liquidity permissionless. Anyone could deposit assets, anyone could trade against the pool, and anyone could build on top of that liquidity.

The liquidity pool exposed a simple pricing formula like `x × y = k`, users traded against it, and price discovery emerged from arbitrage and natural flow. This model is elegant, and today it still solves a problem that active market makers cannot solve cleanly, namely how to provide transparent and always available liquidity for new assets with no reference price and sparse demand. For these long-tail assets, this model remains dominant.

PropAMMs are designed for the markets where execution quality matters most, the short and medium tail of highly traded assets such as BTC, ETH, and SOL. As we argue later in this piece, the model can extend to all onchain markets including prediction markets, perpetual futures, and tokenized securities. The latter of which, we will focus on later. PropAMMs open a wider design space for active trading by allowing book construction, inventory management, and defensive logic to be customized and embedded directly in the onchain program.

What Are PropAMMs

A PropAMM is an onchain program that provides executable bids and offers for a given trading pair. Unlike a passive AMM, where prices follow a fixed mathematical curve and only move when someone trades against the pool, a PropAMM continuously reprices its liquidity based on an offchain pricing model. A user's swap settles directly against the program's onchain liquidity on the blockchain, and the resulting execution is independently verifiable by anyone.

A PropAMM is a two-part system, an offchain pricing engine and an onchain execution program. The offchain engine forms a view of the market by continuously estimating fair value and deciding when that view should be pushed onchain. The onchain program then turns that market view into executable liquidity. The closest analogy here is colocation. In traditional markets, colocation places a trader’s systems physically next to the matching engine yet still requires a round-trip of time to observe, recompute, and submit. A PropAMM goes further. It places core market making logic onchain and by definition inside the exchange's execution environment itself, so book construction, fees, inventory management, and defensive controls can react within the same transaction as the trade.

No two PropAMMs are exactly alike. Each reflects its operator’s own proprietary logic (which is where the name comes from) even if the execution itself is fully onchain and verifiable. In the sections that follow, we focus on the core functions and design patterns shared across many of the PropAMMs competing today, including our own, BisonFi.

The Oracle Update

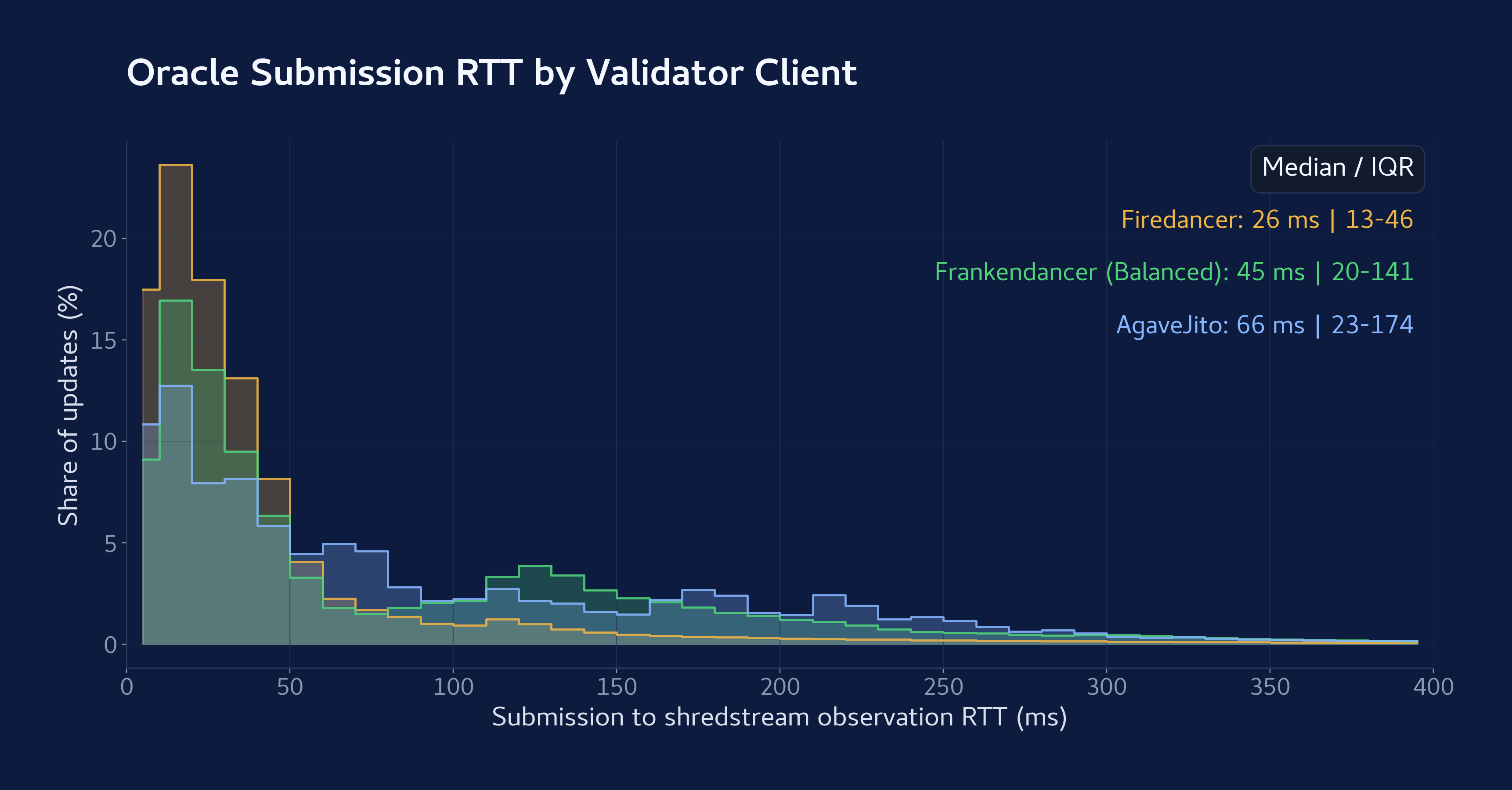

The oracle update is the link between the offchain pricing engine and the onchain execution program. The offchain system watches centralized exchange order books and other venues relevant to the pricing model, continuously recomputes fair value, and pushes those updates to the program as signed transactions. PropAMMs typically submit oracle updates on a fixed cadence, for example every 100 milliseconds, and will update sooner when the fair value moves beyond a configurable threshold from the current onchain reference price.

Each update carries a nonce (a sequence number) for replay protection and ordering. The program rejects updates whose nonce is older than the current onchain counter and, on success, advances that counter to one above the accepted value. Readers familiar with FIX will recognize the parallel to sequence numbering, but where FIX enforces gap-free delivery and retransmission of missed messages, the nonce here does the opposite. Only the freshest update advances the program's state. In practice, this lets operators A/B test different infrastructure paths, transaction fee strategies, or race submission modes to see which may produce the best landing outcomes and under what conditions.

For competitive markets like SOL/USDC, operators need fast inclusion signals confirming that an update has made it into the current block. On Solana, the leader continuously builds the block over roughly a 400ms window, streaming sets of transactions as shreds throughout that window via a protocol called Turbine. Because shreds propagate before the block is complete, the round trip time from oracle submission to observing inclusion can be as short as a few milliseconds depending on the leader’s client software and block-packing logic. The chart below shows BisonFi's observed oracle submission round-trip times across the three major validator clients on Solana for March 2026.

In designs shared across several PropAMMs, including BisonFi, the oracle update is a compact binary payload containing the fields the program needs to refresh its market view, an instruction identifier, a nonce, a fair value estimate, and any optional strategy-specific parameters. It does not transmit a full book snapshot. The onchain program derives the liquidity profile from the current pool reserves and a stored configuration, which is what allows the oracle update to stay small.

The Onchain Book and Strategy

Once the oracle update lands, the program turns it into executable liquidity. In the case of BisonFi, the program constructs a discrete tick book centered on the oracle midpoint. The book has ten levels, five bids and five asks, plus a midprice. Each tick represents a configurable share of pool inventory at a given offset from the oracle, with depth derived from the pool’s current reserves and a predefined target allocation. The oracle update tells the program where the market is. The program decides how much liquidity to show around it.

The book is not static. As trades fill against it, individual ticks can become depleted. Small fills may be replenished atomically within the same block, while larger trades that reach deeper into the book may leave those levels empty as a defensive measure. Each new oracle update then restores depleted ticks toward their baseline allocation, rebuilding depth across the full price ladder. On a centralized exchange, that re-layering loop lives outside the venue, requiring a series of submissions to cancel, recalculate, and repost. Here, it sits inside the execution environment and recalculates atomically with each new trade or oracle update.

The program also controls how aggressively the pool trades under different conditions. When the pool drifts away from its target balance, the program will typically encourage rebalancing flow by showing more liquidity on the side where inventory is short and less on the side where it is long. It will also penalize trades that push inventory further out of line by widening the relevant price offset.

Freshness and flow quality are another dimension of that control. When the market view is fresh and incoming flow appears benign, a swap may see the full standard book. When several blocks have passed since the last oracle update or if the swap arrives through a routing path associated with adverse selection, the program can respond defensively. Defenses include widening fees, withholding depth at certain ticks, inspecting the swap payload to identify and penalize toxic takers, and scoring routing paths by the historical quality of their flow. The result is a book that adapts not just to price and inventory, but also to time and flow quality.

Comparative Trading Outcomes

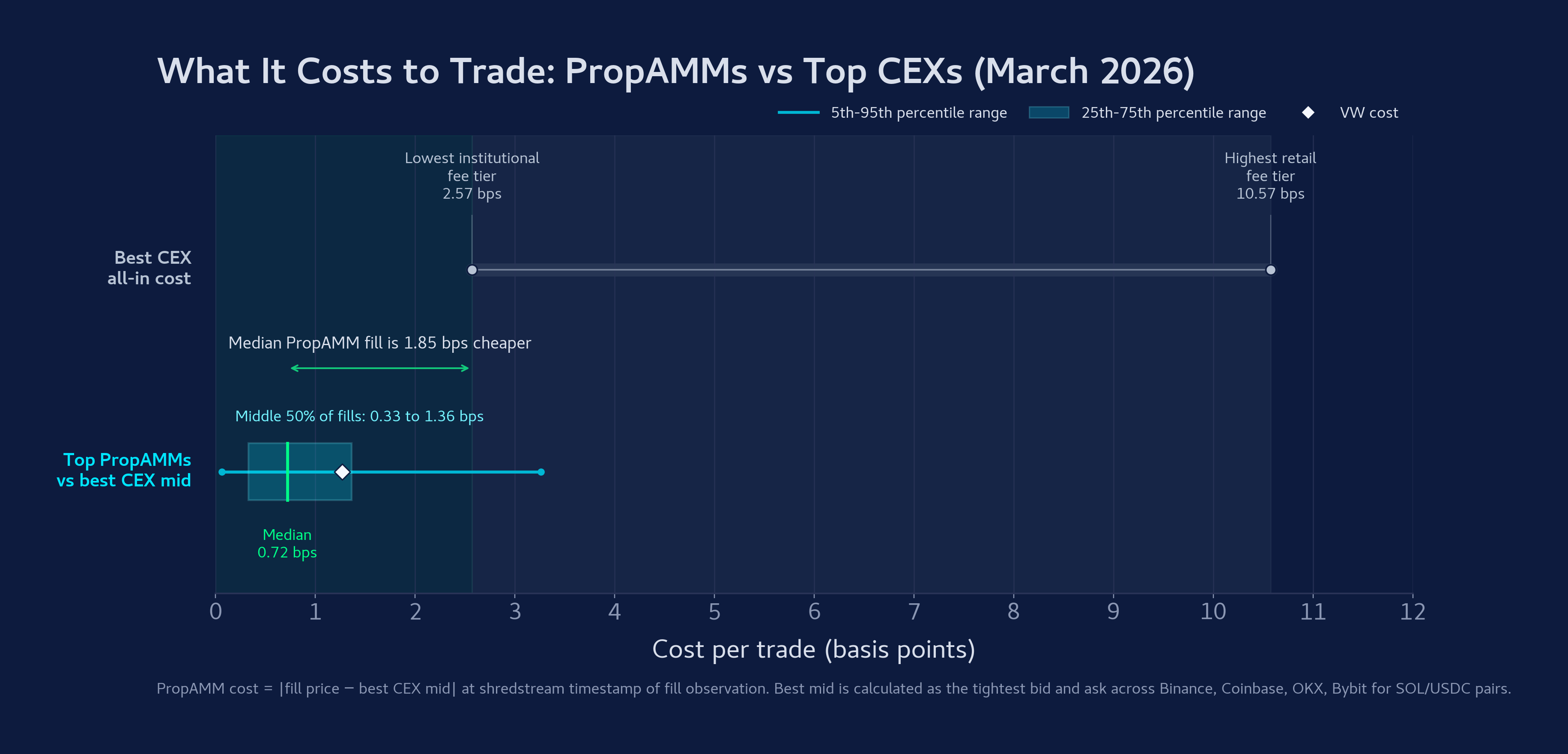

Across the top PropAMM cohort on Solana, the median SOL/USDC fill executed 0.72 bps from the best midpoint across the top centralized exchanges. To construct that reference, we captured tick-level top-of-book data from Binance, Coinbase, OKX, and Bybit at the nanosecond timestamp of every PropAMM fill observed across our shredstream proxies to construct the tightest bid and ask across all four venues. The resulting midpoint is the most favorable reference price any of these exchanges could offer at that given moment.

On a centralized exchange, takers are required to pay the spread plus an exchange fee on every fill. At the most favorable tiers available, ones that often require several billion per month in volume to qualify, the all-in cost is 2.57 bps. Against that line, 91.9% of PropAMM fills and 90.2% of total notional were cheaper for end users. At the lowest retail tier, the all-in cost runs above 10 bps, and 99.3% of PropAMM fills beat it.

It’s important to note that some aggregators and wallet frontends charge fees on swaps, while others do not. These fees are not structural to PropAMM execution itself but to the specific aggregator or interface a user may choose. For the purposes of this comparison, we measure PropAMM execution cost at the protocol level, which is the price any user can access through free frontends or aggregators.

These results hold across the full distribution, not just at the median. Over the 20 million fills we analyzed across March 2026, the middle 50% of PropAMM fills landed between 0.33 and 1.36 bps from our calculated best CEX mid. PropAMMs did not simply match centralized venue pricing, they beat it across nearly every fill in the sample.

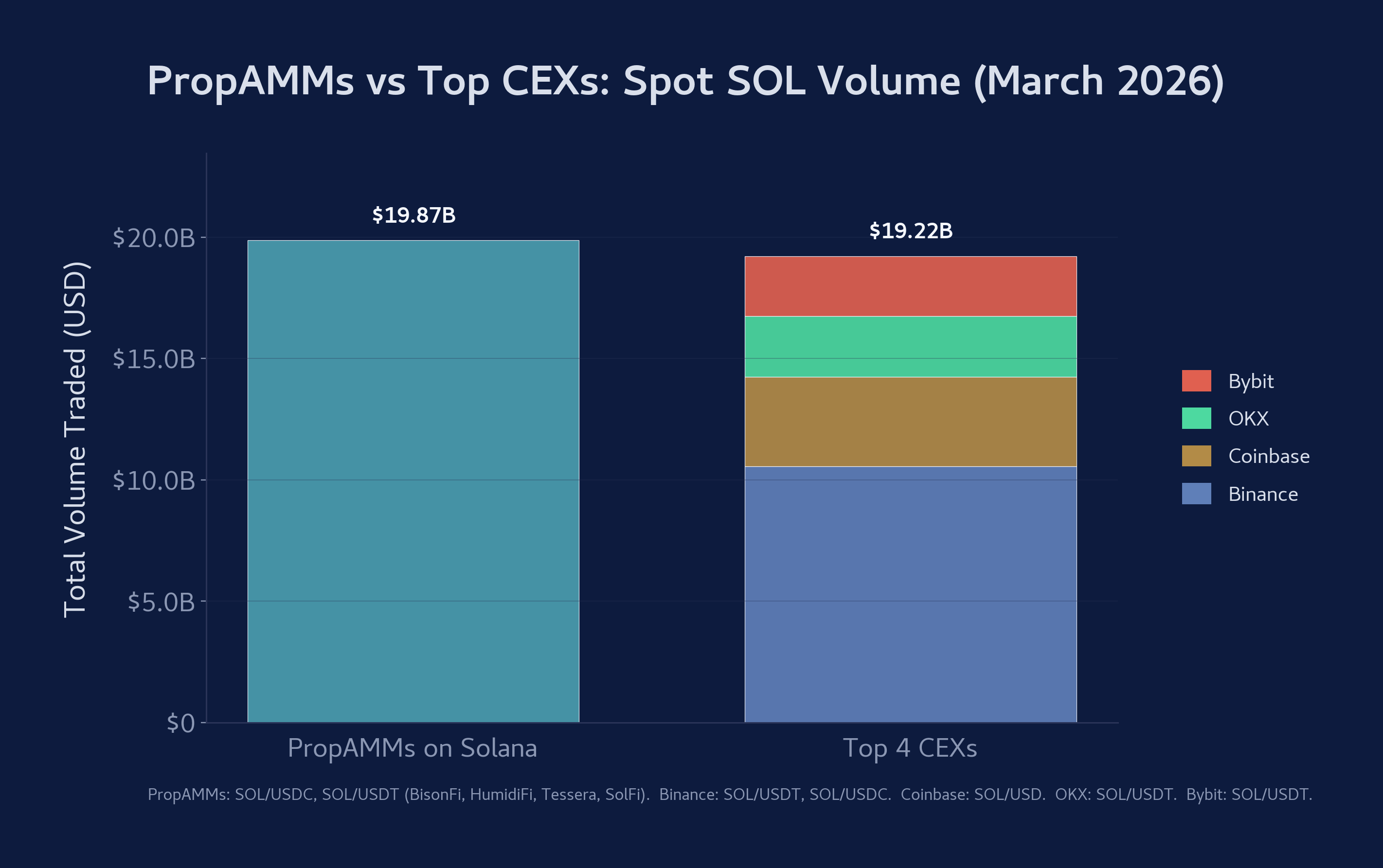

This wasn't some niche segment of the SOL spot market. Onchain volume for March across the top PropAMM cohort on Solana totaled $18.19 billion in SOL/USDC and $1.68 billion in SOL/USDT, for a combined $19.87 billion across the two pairs.

For that same period, the top four centralized exchanges recorded $10.56 billion (Binance, split $8.77 billion in SOL/USDT and $1.79 billion in SOL/USDC), $3.67 billion (Coinbase), $2.52 billion (OKX), and $2.46 billion (Bybit) across their SOL dollar pairs, totaling $19.22 billion combined. PropAMM volume matched the aggregate of all four.

Why this happens

PropAMMs operate in an environment of perfect competition against each other and other sources of onchain liquidity for flow from aggregators. If one operator quotes wide, aggregators will simply direct flow to the tighter source of liquidity. This kind of open, permissionless competition simply does not exist on centralized venues, where access to provide liquidity is gated and numerous rent extracting intermediaries exist. On Solana, the only barrier to PropAMM entry is writing better code and quoting a better price.

MEV and Competition for Blockspace

The magnitude of this outperformance may surprise observers familiar with the critique that permissionless blockchains suffer from extractive behaviors such as sandwich attacks or validator discretion in transaction inclusion and ordering broadly labeled as "MEV." The topic is broad, but two specific concerns are most relevant to PropAMMs.First, that retail traders will see fills worse than the market's best possible offer. Second, that market makers will be exposed to adverse selection on blocks where validators reorder or censor oracle updates.

For PropAMMs market makers, transaction ordering discretion and censorship by validators are real concerns for operators. An oracle update that lands late exposes the PropAMM to adverse selection. PropAMMs aim to mitigate this with the staleness and toxicity protections we described above: spreads widen, depth is withheld as block age increments, and certain traders or types of flow that periodically exploit that staleness are explicitly penalized.

These concerns around "MEV" costs, however, still need to be measured against what market makers actually pay in the traditional systems with which PropAMMs compete. Colocation fees, negotiated fee tiers, queue priority competition, and latent data access serve the same function in traditional markets, paying for execution priority in a system where latency determines winners and losers. The difference is that those costs are invisible to every participant who doesn't have them and are controlled by centralized gatekeepers. Priority fees on transactions shift execution advantages to an open, transparent, and verifiably competitive auction building a democratized mechanism for its access.

The Solana community recognizes the opportunity to further innovate on market structure while also mitigating what’s left of these “MEV” costs. Immediate term proposals aimed at dropping block times from 400ms to 200ms shrink the maximum staleness window PropAMMs are exposed to. Shorter leader rotations, from four blocks to two, further reduces the window's exploitable economic surface area. A 50ms market tick introduces an even more granular onchain notion of time within a block, letting PropAMMs distinguish a 50ms old quote from a 100ms one to price defensively with corresponding precision. Shifting transaction ordering in-protocol by priority fee relative to compute units gives market participants the same fair and deterministic rules for competing on inclusion and ordering.

For retail users, PropAMM fills established pairs already deliver better all-in execution relative to centralized and permissioned exchanges. Residual variance between a quoted price and the realized fill can still arise from latency between quote display and transaction landing. Onchain routers largely close this gap by resolving the best executable price across all available liquidity sources at the moment the transaction is executed, not at the moment the user initiates the swap.

PropAMMs also significantly reduce the attack surface that passive AMMs are exposed to. Sandwich attacks work by exploiting a trader's slippage tolerance (the maximum price deviation a user will accept on their swap), buying before the victim to push the price up, then selling into the pool after. For established pairs on PropAMMs, the frequency of intra-block oracle updates and the tightness of spreads across the book compress the potential margin of such attacks, often below the cost of executing them. And because onchain aggregators evaluate all available liquidity sources at the moment a user's transaction executes, flow can be routed to competing sources of liquidity entirely.

No market structure eliminates every inefficiency. But the data already shows PropAMMs outperforming centralized venues on the metrics that matter most, and we believe near-term protocol improvements on Solana's roadmap will widen that advantage further.

Interface Disclosures

We appreciate and are supportive of the recently released staff statement by the SEC’s Division of Trading and Markets around user interfaces providing access to crypto asset securities. We are particularly supportive of references made to user interfaces using software “that operates based on pre-disclosed and objective parameters that are independently verifiable.” The benefits of the PropAMM model are best realized when aggregation logic is fully onchain. Additionally, as noted in the staff statement, frontend interfaces should provide user controllable slippage parameters as a backstop to the inherent benefits in a PropAMM market structure.

Tokenized Securities

The previous sections demonstrate that PropAMMs can deliver superior execution quality for spot crypto pairs on Solana. We believe this model is not limited to spot crypto pairs and that it will be particularly well suited to tokenized securities. The core function of a PropAMM is largely asset-class agnostic and can be deployed with minimal changes necessary.

What does change is the regulatory environment, which is both the obstacle and the opportunity. To understand why, we will briefly cover an aspect of US equity market structure that is already under active reconsideration.

Reg NMS

Regulation National Market System (Reg NMS), adopted by the SEC in 2005, was the most significant structural reform to US equity markets in decades. Its primary objectives were straightforward: ensure that investors receive the best available price, promote fair competition among trading venues, and modernize the infrastructure through which quotes and trades are disseminated.

The central component of Reg NMS is the Order Protection Rule (Rule 611), which established the concept of "protected quotes." Under this rule, a trading venue cannot execute an order that is worse than the best displayed price on another venue that is part of the national market system. This best displayed price, aggregated across all participating venues, is the National Best Bid and Offer (NBBO). In practice, the rule means that if NYSE is showing a bid of $100.01 and Nasdaq is showing a bid of $100.02, a sell order arriving at NYSE cannot be executed at $100.01 without first attempting to route to or match the $100.02 bid on Nasdaq. NBBO is disseminated through the Securities Information Processors (SIPs), consolidated data feeds that aggregate quotes from all protected venues.

The intent was to ensure that fragmentation across venues did not harm investors by allowing trades to execute at inferior prices when better prices were available elsewhere. The mechanism was to create a consolidated, continuously updated reference price that all venues were obligated to respect.

The results since enactment have been mixed, and the criticisms are well-documented. Reg NMS did not reduce fragmentation, it accelerated it. By guaranteeing that any venue displaying a protected quote would receive order flow routed to it under Rule 611, the rule lowered the barrier to launching new trading venues. The number of exchanges with protected quotes has more than tripled since enactment. Each new venue adds complexity to routing, introduces new fee structures, rebate tiers, and creates additional infrastructure dependencies while offering minimal differentiating innovation.

SEC Chair Paul Atkins has acknowledged these structural concerns directly, noting the increasing complexity of a system that was designed for a much simpler venue landscape. The PTG, representing many of the largest trading firms (including Jump), has argued in its position paper for a number of targeted reforms to Reg NMS including the repeal of Rule 611 and adopting a disclosure and principles-based approach to best execution. The SEC has signaled openness to modernizing Reg NMS, though the form that changes may take remains uncertain.

We believe PropAMMs are well-suited for providing liquidity to tokenized securities for reasons that go beyond simply replicating existing markets on blockchain settlement rails. As a matter of fact, the structural properties of PropAMMs on permissionless blockchains address several of the specific problems that Reg NMS was designed to solve and that some argue it has failed to solve adequately.

Execution quality and price improvement. As the data in this piece demonstrates, PropAMMs on Solana are already delivering total cost of execution that are competitive with, and in many cases superior to, the largest centralized venues. For highly liquid equities, the offchain pricing engine has even richer inputs to work with. PropAMMs for tokenized equities would have access to the same reference pricing (such as NBBO) that informs market makers on existing equities venues.

On a PropAMM, the same economic function, referencing offchain price sources and competing to offer price improvement, would occur on a public ledger where every individual execution is independently verifiable.

PropAMM's offer transparency that exceeds current reporting requirements. Today, Rule 605 requires market centers to publish execution quality statistics aggregated by order type and size category. Rule 606 requires brokers to disclose their routing practices and payment-for-order-flow arrangements on a quarterly basis. These disclosures are aggregated and delayed to where meaningful comparison across venues requires significant effort. A retail investor cannot easily determine, after the fact, whether their specific order received the best available execution or whether their broker's routing decisions were optimal.

On a permissionless blockchain, every oracle update and trade executed by every PropAMM is recorded immutably. A regulator does not need to request it through a compliance department. A retail investor does not need to wait for a quarterly report. An independent analyst can compute price execution quality (improvement or disimprovement) for every individual trade against the NBBO as a reference. This evaluation of execution could easily adapt to any changes to Reg NMS and how best execution is measured leading to new potential ways of market oversight.

Moving Forward, Not Backward

We want to be explicit about the importance of permissionless blockchains in this thesis, because it is the point on which we feel most strongly and which invites the most skepticism from some market participants. A permissioned blockchain is a database with extra steps; it inherits none of the public verifiability, composability, or open competition that make blockchains useful as market infrastructure. Closed systems also carry the risk of following a pattern seen across finance and tech: early subsidized access that, once users are locked in, gives way to higher fees, tighter controls, and defended moats. Credibly neutral infrastructure built upon a globally distributed consensus removes that single point of unilateral authority, giving certainty for those bringing markets onchain. Institutional capital will move onchain because of these permissionless features, not in spite of it. The history of forking open source protocols serves as a natural check on rent seeking behavior and an incentive to innovate. A developer is free to take existing open source code and apply alternative market designs such as the Dual Flow Batch Auction we’ve previously proposed.

Compliance does not require a permissioned blockchain, neither do market participants. If required, transfer restrictions, KYC/AML gating, and jurisdictional controls can all be enforced at the token contract and asset layer while settlement remains open, verifiable, and composable. On a permissionless chain, every trade is recorded in real time with data immutably available to regulators, institutions, and retail participants alike to independently verify.

PropAMMs today operate in spot crypto markets on Solana. They are competing against other sources of onchain liquidity, centralized exchanges, and each other. They are winning that competition on execution quality and doing so in a way that is measurable and verifiable. The natural extension of PropAMMs to other asset classes including tokenized securities, perpetual futures, and prediction markets is not a leap but a natural next step. One that requires adapting a microstructure model that works and thoughtful engagement with regulators.